• MPR may see another policy rate increase

• Manufacturers borrowing at 35 per cent

• Money supply doubles in 24 months despite restraint

• ‘High cost of borrowing pushing up price, worsening employment’

• Inflation up 2% since last meeting, members’ notes point to prolonged hike

The question of whether to raise or hold the monetary policy rate (MPR) confronts the Monetary Policy Committee, the rate-fixing arm of the Central Bank of Nigeria (CBN), as its members converge on Abuja in the next two days for its crucial 295th meeting.

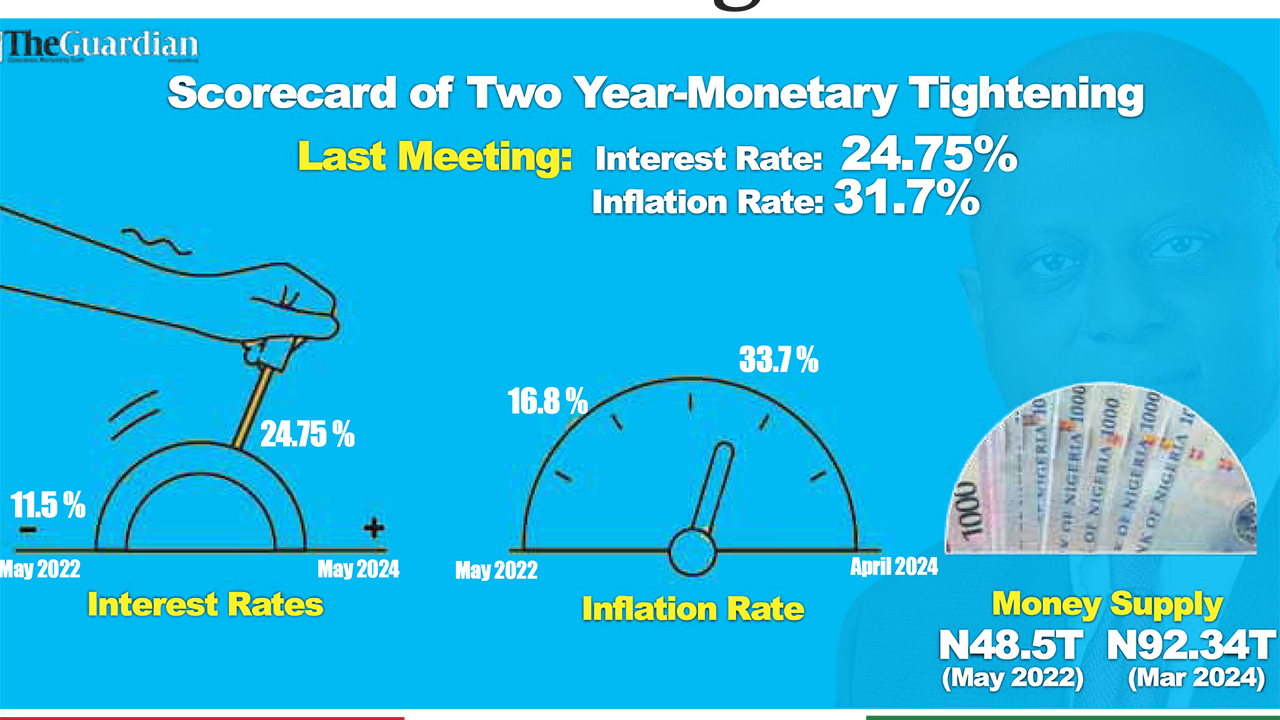

As in the past two years, a rate cut is not an option even though the broader economy thinks it is time to consider that. With the headline inflation in near a three-decade high (33.7 per cent), the monetary authority is not expected to moderate the two-year-old monetary tightening, which has raised the anchor interest rate from 11.5 per cent to 24.75 per cent or 115 per cent.

The aggressive tightening has increased the burden of funds on individuals and corporate entities, contributing to the downside factor weighing on local production and calling for some restraint.

In the past two years, inflation has doubled (from 16.82 per cent in April 2022 to 33.7 per cent last month), assuming an increasing function of the interest rate contrary to expectation. Experts have, thus faulted the efficiency of the tightening campaign and called for restraint.

However, the Central Bank has argued that the inflation rate would be worse with a loose monetary environment. Rather than heed dissenting views, the MPC has doubled down on its money supply tightening in the past two meetings supervised by Yemi Cardoso, increasing the MPR by six per cent. That has taken the interest rate to the highest in recent history.

With some economists already projecting a 1.5 per cent hike in meeting decisions due for an announcement tomorrow, there are no signs the tightening exercise has peaked.

An economist and Director General of the Centre for Promotion of Private Enterprise (CPPE), Dr Muda Yusuf, has warned repeatedly about the dire consequences of further tightening for the competitiveness of the local manufacturers, who have turned to commercial banks to borrow at over 30 per cent interest rate.

In March, CBN data pegged the maximum lending rate at 29.38 per cent. But borrowers said fresh facilities are sealed at over 35 per cent in some cases, even as odds increase with risk re-pricing.

Unbending interest shows two-year rake hike run only means more pain for manufacturers whose assets are eroded by rising inflation while they also borrow at cut-throat prices.

Money supply has equally remained upbeat, doubling in the past two years. For instance, broad money balances have increased from N48.51 trillion in May 2022 to N92.34 trillion in March 2024. With much of the money creation coming from the CBN quantitative easing (including illegally administered Ways and Means facilities), some experts have blamed the CBN, under Godwin Emefiele, for the stubbornly high inflation.

In principle, there is a policy trade-off between inflation (and money supply) and interest rates such that the former is a decreasing function of the latter. The theory has been validated by the interaction between the two variables in Europe and the United State s in the past two years.

For one, the inflation rate was over eight per cent in March 2022 when the Federal Reserve first raised the interest slightly above near zero at the beginning of its recent tightening policy. The inflation rate has climbed down to below 3.5 per cent. Sadly, Nigeria’s inflation rate has risen neck-in-neck with interest rate, raising questions about the policy relevance of the MPC’s decision.

The slight drop in broad money from N95.56 trillion to N92.34 trillion in March may have given the CBN some sense of success and emboldened its open-ended interest rate campaign, suggesting another hike could be handed down to the bleeding economy tomorrow.

While raising rates is aimed at controlling inflation by making borrowing more expensive, it discourages investments, cripples agreement demand and increases unemployment as it feeds into commercial loans and credit purchases.

As the monetary authority continues to adopt and restrict the growth of the money base to tackle inflation, some stakeholders have demanded special attention be given to critical sectors of the economy through tailored development financing, a suggestion that may not have appealed to Cardoso, who has expressed commitment to conventional monetary policy.

They also said the naira may be sliding because of the uncertainties around the monetary and fiscal policies and do “everything necessary to bring inflation down”.

With the yield curve differential which currently stands at 9.15 per cent and the headline inflation up by 2.69 per cent since the last MPC meeting, an economist, Kelvin Emmanuel, said he expects the MPC to raise the rate by 150 basis points from the current 24.75 to 26.25 tomorrow when the MPC meeting concludes its deliberations.

He explained: “I expect that the 295th meeting will result in a 150-basis point hike from 24.75 per cent to 26.25 per cent. However, on a month-by-month basis, we can see a slowdown of increase, so I expect that the inflation rate increase will peak in June and the July reading from the NBS will show a plateau.”

Emmanuel agreed that raising the rates will not solve Nigeria’s economic challenges, saying: “I think the government needs to focus on raising its revenue to a gross domestic product (GDP) ratio that will migrate the fiscal strategy paper from debt to revenue while renegotiating concessionary loans to reduce the amount of debt servicing and refinancing cost while bringing down the deficit financing from above 40 per cent to below 30 per cent”.

He added that the most veritable achievement of achieving this is to transfer beneficial ownership of oil and gas assets to an asset manager to administer.

“The Senate Committee on Banking needs to act quickly to pass the proposed amendment of the 2007 CBN Act in Sections 38 that seeks to tie FG’s share of FAAC revenues as collateral in an irrevocable payment standing order (ISPO) to ways and means advances from the Central Bank to the FG as a tool to prevent abuse of the newly-proposed 10 per cent of real revenues for the previous accounting year. And this is because, other than the low access to credit from high-interest rate and CRR, the money supply is a major glut in the cost-push input to the accelerating inflation rate we are seeing,” he said.

Other experts noted that Nigeria’s current economic crisis is multifaceted and that all authorities need to tread with caution to prevent tipping the economy into a deeper crisis.

A professor of economics at Lead City University, Godwin Oyedokun, said there is no easy solution and called on the MPC to weigh carefully the trade-offs involved in its decision.

“But a comprehensive, coordinated policy approach stands the best chance of bringing inflation under control without unduly harming the economy,” he said, advising the fiscal authority to support low-income households to offset the impact of higher prices.

“Of course, there should be coordination between monetary and fiscal policies to tackle the multi-faceted challenge of persistent inflation. The MPC and fiscal policymakers should work closely to ensure their policies are aligned and complementary,” the professor stated.

The insistence by the CBN governor to keep the rates high for as long as it is necessary to force down inflation is already sending shivers down the spine of manufacturers, different groups in the manufacturing value chain have warned.

The President of the Lagos State Chapter of the Association of Certified Fraud Examiners (ACFE), Dr Titilayo Fowokan, said the implications of the insistence mean higher borrowing costs, which will discourage borrowing for investment.

“This will have the ultimate effect of slowing down economic activities. The rise in MPR is expected to encourage savings, but the citizens are still trying to survive from previous economic shocks of removal of fuel subsidy and exchange rate unification,” she explained.

Fowokan said the MPC needs to consider an MPR reduction or keep it at the level as long as it does not exacerbate the worsening inflation, especially in the food segment.

She warned: “Any further strain on the economy could move more citizens into poverty and businesses to extinction,” adding that reduction in MPR would be advantageous at this stage as the cost of living is rather on the high side.

For Yusuf, it is a delicate matter that demands that the CBN do a cost-benefit analysis to see if the benefits of high interest rates outweigh the disadvantages.

“For me keeping the interest rates high could significantly hurt the economy,” he said. In her notes at the last MPC meeting, a member, Aku Pauline Odinkemelu, stressed the urgent need for the government to increase its revenue and block leakages.

She expressed anxiety over Nigeria’s debt stock, saying: “Anticipated fiscal deficit of N9.18 trillion is swelling the already existing debt stock of N87.91 trillion and N96.43 trillion by the end of 2024. Achieving sustainable growth in 2024, therefore, entails a delicate balancing of ambitious fiscal reforms with effective budget implementation, while the monetary authority is expected to promote price stability.”

Odinkemelu gave a hint on why the CBN may likely keep rates up for the near future. She said that the rise in the inflation rate from 29.9 per cent in January to 31.7 per cent in February “means that the CBN cannot fold its arms and do nothing”.